NAR: Pending Home Sales Rose 0.3% in June, First Increase in Four Months

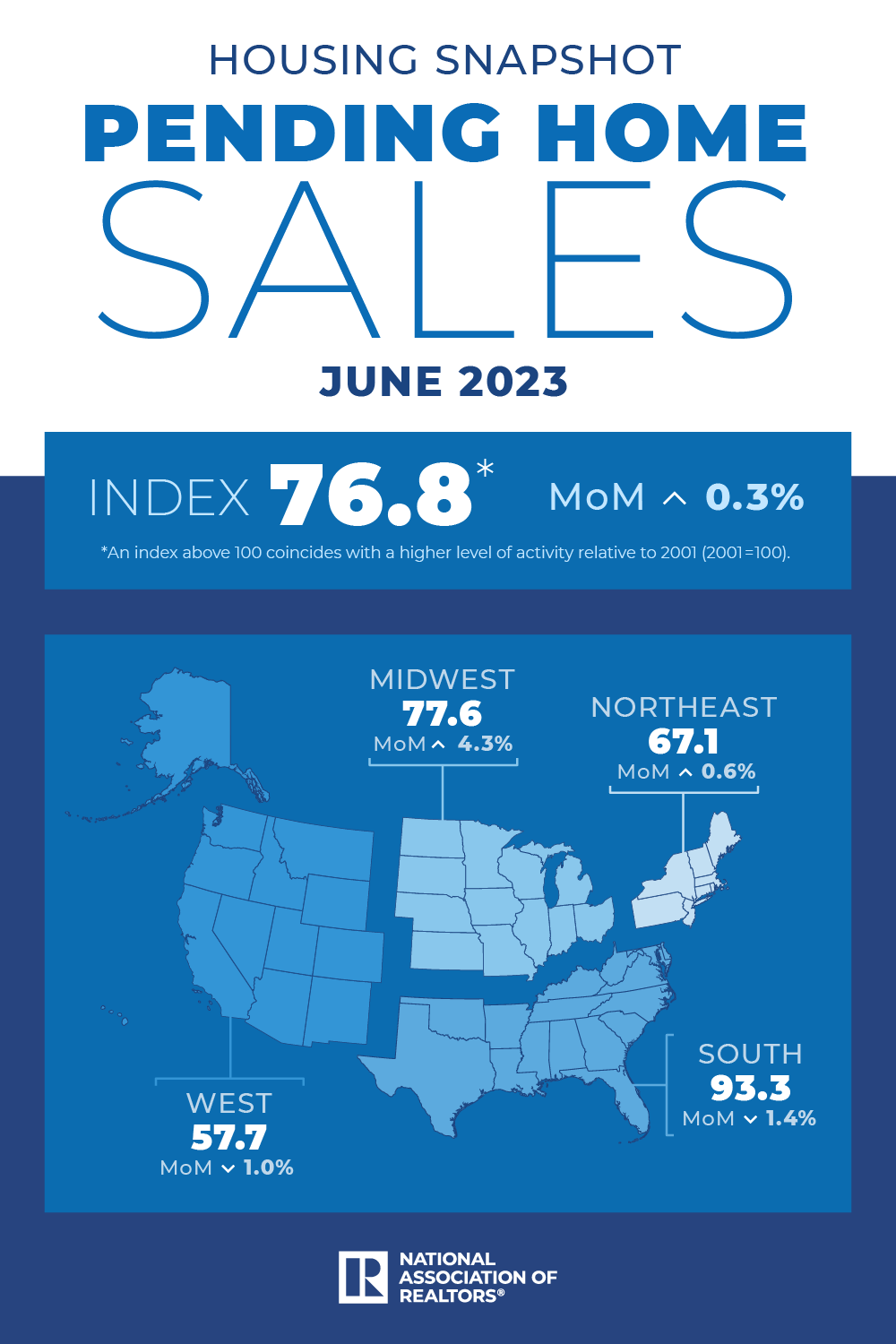

Pending home sales registered a modest increase of 0.3% in June from the previous month – the first increase since February – according to the National Association of REALTORS®. The South and West posted monthly losses, while sales in the Northeast and Midwest grew. All four U.S. regions saw year-over-year declines in transactions.

Key Highlights

- Pending home sales augmented in June, up 0.3% from May.

- Month over month, contract signings increased in the Northeast and Midwest but decreased in the South and West.

- NAR forecasts the 30-year fixed mortgage rate will hit 6.4% in 2023, followed by 6.0% in 2024. While median home sales will decrease 12.9% from 2022 to 2023 (4.38 million), they will climb 15.5% in 2024 (5.06 million).

“The recovery has not taken place, but the housing recession is over,” said NAR Chief Economist Lawrence Yun, “The presence of multiple offers implies that housing demand is not being satisfied due to lack of supply. Homebuilders are ramping up production and hiring workers.”

The Pending Home Sales Index (PHSI)* – a forward-looking indicator of home sales based on contract signings – rose 0.3% to 76.8 in June. Year over year, pending transactions fell by 15.6%. An index of 100 is equal to the level of contract activity in 2001.

NAR forecasts that the 30-year fixed mortgage rate will hit 6.4% this year and then decline to 6.0% in 2024, while the unemployment rate will rise slightly to 3.7% in 2023 before increasing to 4.1% in 2024.

“With consumer price inflation calming close to the Federal Reserve’s desired conditions, mortgage rates look to have topped out,” Yun added. “Given the ongoing job additions, any meaningful decline in mortgage rates could lead to a rush of buyers later in the year and into the next.”

NAR expects existing-home sales to decrease 12.9% from 2022 to 2023, settling at 4.38 million, before climbing 15.5%, to 5.06 million in 2024. Compared to last year, national median existing-home prices will remain steady – declining 0.4%, to $384,900, before rebounding by 2.6% next year, to $395,000. The West – the country’s most expensive region – will see reduced prices while the more affordable Midwest region is likely to see a small, positive increase. Housing starts will drop 5.3% from 2022 to 2023, to 1.47 million, before increasing to 1.55 million, or 5.4%, in 2024.

“It is critical to expand supply as much as possible to widen access to homebuying for more Americans,” Yun said. “Home prices will be influenced by how much inventory is brought to market. Increased homebuilding will tame price growth, while limited construction will lead to home price appreciation outpacing income growth.”

Newly constructed home sales will increase from last year by 12.3% in 2023, to 720,000 – due to additional inventory in this segment of the market – and increase by another 13.9% in 2024, to 820,000. The national median new home price will decrease by 1.9% this year, to $449,100, and then improve by 4.2% next year, to $468,000.

Pending Home Sales Regional Breakdown

The Northeast PHSI ascended 0.6% from last month to 67.1, a decrease of 16.7% from June 2022. The Midwest index jumped 4.3% to 77.6 in June, down 17.1% from one year ago.

The South PHSI receded 1.4% to 93.3 in June, lessening 14.3% from the prior year. The West index fell 1.0% in June to 57.7, dipping 15.5% from June 2022.

About the National Association of REALTORS®

The National Association of REALTORS® is America’s largest trade association, representing more than 1.5 million members involved in all aspects of the residential and commercial real estate industries. The term REALTOR® is a registered collective membership mark that identifies a real estate professional who is a member of the National Association of REALTORS® and subscribes to its strict Code of Ethics.

# # #

*The Pending Home Sales Index is a leading indicator for the housing sector, based on pending sales of existing homes. A sale is listed as pending when the contract has been signed but the transaction has not closed, though the sale usually is finalized within one or two months of signing. Pending contracts are good early indicators of upcoming sales closings. However, the amount of time between pending contracts and completed sales is not identical for all home sales. Variations in the length of the process from pending contract to closed sale can be caused by issues such as buyer difficulties with obtaining mortgage financing, home inspection problems, or appraisal issues. The index is based on a sample that covers about 40% of multiple listing service data each month. In developing the model for the index, it was demonstrated that the level of monthly sales-contract activity parallels the level of closed existing-home sales in the following two months. An index of 100 is equal to the average level of contract activity during 2001, which was the first year to be examined. By coincidence, the volume of existing-home sales in 2001 fell within the range of 5.0 to 5.5 million, which is considered normal for the current U.S. population.

NOTE: Existing-Home Sales for July will be reported on August 22. The next Pending Home Sales Index will be on August 30. All release times are 10 a.m. Eastern. View the NAR Statistical News Release Schedule.

Contact:

Lauren Cozzi – Media Contact – (202) 383-1178

Source: National Association of Realtors

The Value of Membership

As the leading provider of in-depth business and credit information on the domestic lumber & forest products industry, a membership with Blue Book Services gives you access to:

- Ratings & Business Reports

- Dynamic Search Tools

- Real-Time Data