Rayonier Reports Second Quarter 2023 Results

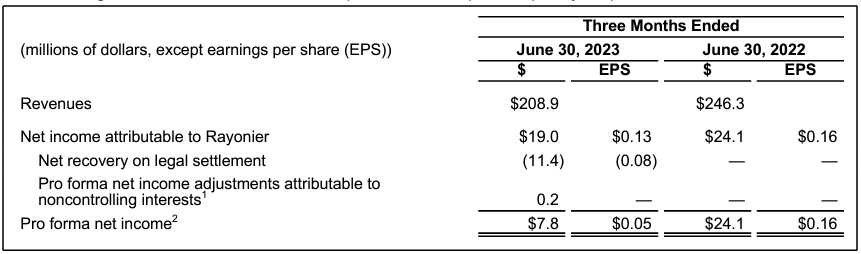

Rayonier Inc. (NYSE:RYN) today reported second quarter net income attributable to Rayonier of $19.0 million, or $0.13 per share, on revenues of $208.9 million. This compares to net income attributable to Rayonier of $24.1 million, or $0.16 per share, on revenues of $246.3 million in the prior year quarter.

The second quarter results included an $11.4 million net recovery associated with a legal settlement. Excluding this item and adjusting for pro forma net income adjustments attributable to noncontrolling interests,1 second quarter pro forma net income2 was $7.8 million, or $0.05 per share.

The following table summarizes the current quarter and comparable prior year period results:

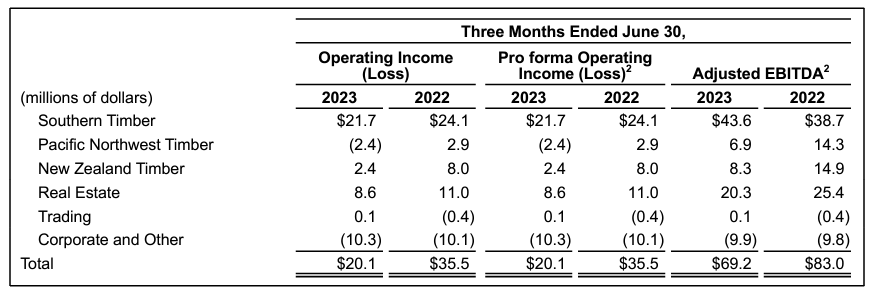

Second quarter operating income was $20.1 million versus $35.5 million in the prior year period. Second quarter Adjusted EBITDA2 was $69.2 million versus $83.0 million in the prior year period.

The following table summarizes operating income (loss), pro forma operating income (loss),2 and Adjusted EBITDA2 for the current quarter and comparable prior year period:

Year-to-date cash provided by operating activities was $126.3 million versus $148.5 million in the prior year period. Year-to-date cash available for distribution (CAD)2 was $62.7 million, which decreased $56.8 million versus the prior year period due to lower Adjusted EBITDA2 ($57.1 million), higher capital expenditures ($6.5 million) and higher cash interest paid ($3.8 million), partially offset by lower cash taxes paid ($10.6 million).

“While overall market sentiment has improved versus the first quarter of this year, our second quarter results reflect ongoing macroeconomic challenges and weaker end-market demand as compared to the prior year,” said David Nunes, CEO. “The total Adjusted EBITDA generated by our Timber segments collectively declined 13% relative to the second quarter of 2022, as favorable results in our Southern Timber segment were more than offset by lower Adjusted EBITDA in our Pacific Northwest Timber and New Zealand Timber segments.”

“In our Southern Timber segment, Adjusted EBITDA improved by $4.9 million as harvest volumes increased 32% relative to the prior year quarter, primarily due to the successful integration of the acquisitions completed in late 2022. The higher volumes were partially offset by a 14% decline in weighted-average net stumpage prices due to weaker demand and drier weather conditions as compared to the prior year period.”

“In our Pacific Northwest Timber segment, Adjusted EBITDA declined $7.4 million from the prior year quarter as weaker domestic markets coupled with less competition from export markets drove a 19% decline in domestic sawtimber prices versus the prior year period. Harvest volumes declined 11% relative to the prior year quarter as we deferred some planned harvests in response to weaker market conditions.”

“In our New Zealand Timber segment, Adjusted EBITDA declined $6.6 million versus the prior year quarter due to lower carbon credit sales, lower net stumpage realizations, unfavorable foreign exchange impacts, and 4% lower harvest volumes as compared to the prior year period.”

“Real Estate segment Adjusted EBITDA was $5.1 million below the prior year quarter, as higher weighted- average per-acre prices in the current quarter were more than offset by 20% fewer acres sold.”

Southern Timber

Second quarter sales of $68.3 million increased $2.0 million, or 3%, versus the prior year period. Harvest volumes increased 32% to 2.01 million tons versus 1.52 million tons in the prior year period, primarily driven by the additional volume contribution from the U.S. South acquisitions completed at the end of 2022. Average pine sawtimber stumpage realizations decreased 15% to $29.07 per ton versus $34.09 per ton in the prior year period, primarily due to drier weather conditions, weaker demand from sawmills, and decreased competition from pulp mills for chip-n-saw volume. Average pine pulpwood stumpage realizations decreased 26% to $15.78 per ton versus $21.46 per ton in the prior year period as weaker end-market demand, drier weather conditions, and extended maintenance outages at pulp mills all contributed to softer market conditions.

Overall, weighted-average stumpage realizations (including hardwood) decreased 14% to $21.85 per ton versus $25.55 per ton in the prior year period. Operating income of $21.7 million decreased $2.4 million versus the prior year period due to lower net stumpage realizations ($7.4 million), higher depletion rates ($2.6 million), and higher overhead and other costs ($1.0 million), partially offset by higher volumes ($7.6 million) and higher non-timber income ($1.0 million).

Second quarter Adjusted EBITDA2 of $43.6 million was 13%, or $4.9 million, above the prior year period.

Pacific Northwest Timber

Second quarter sales of $32.3 million decreased $6.8 million, or 17%, versus the prior year period. Harvest volumes decreased 11% to 332,000 tons versus 376,000 tons in the prior year period as some planned harvests were deferred in response to soft market conditions. Average delivered prices for domestic sawtimber decreased 19% to $97.37 per ton versus $120.44 per ton in the prior year period due to weaker domestic and export market demand. Average delivered pulpwood prices decreased 20% to $36.21 per ton versus $45.17 per ton in the prior year period as the prior year period benefited from much more favorable end-market demand. An operating loss of $2.4 million versus operating income of $2.9 million in the prior year period was driven by lower net stumpage realizations ($5.9 million), lower volumes ($0.8 million) and higher costs ($0.5 million), partially offset by higher non-timber income ($1.1 million) and lower depletion rates ($0.8 million).

Second quarter Adjusted EBITDA2 of $6.9 million was 52%, or $7.4 million, below the prior year period.

New Zealand Timber

Second quarter sales of $60.9 million decreased $18.0 million, or 23%, versus the prior year period. Harvest volumes decreased 4% to 673,000 tons versus 703,000 tons in the prior year period, as some planned harvests were deferred in response to soft market conditions. Average delivered prices for export sawtimber decreased 26% to $103.81 per ton versus $140.44 per ton in the prior year period, driven by increased salvage volume from Cyclone Gabrielle and weaker demand in China; however, export sawtimber net stumpage realizations were relatively flat due to significantly lower port and freight costs versus the prior year period. Average delivered prices for domestic sawtimber declined 10% to $69.29 per ton versus $76.82 per ton in the prior year period. The decrease in domestic sawtimber prices (in U.S. dollar terms) was primarily driven by the decline in the NZ$/US$ exchange rate (US$0.62 per NZ$1.00 versus US$0.66 per NZ$1.00). Excluding the impact of foreign exchange rates, domestic sawtimber prices decreased 3% versus the prior year period, reflecting weaker domestic demand and decreased competition from export markets. Operating income of $2.4 million decreased $5.6 million versus the prior year period due to lower carbon credit sales ($2.8 million), lower net stumpage realizations ($1.5 million), unfavorable foreign exchange impacts ($1.0 million), and lower volumes ($0.5 million), partially offset by lower depletion rates ($0.2 million).

Second quarter Adjusted EBITDA2 of $8.3 million was 44%, or $6.6 million, below the prior year period.

Real Estate

Second quarter sales of $32.0 million decreased $2.4 million, or 7%, versus the prior year period, while operating income of $8.6 million decreased $2.4 million versus the prior year period. Sales and operating income decreased versus the prior year period primarily due to a lower number of acres sold (3,754 acres sold versus 4,694 acres sold in the prior year period), partially offset by a slight increase in weighted-average prices ($7,489 per acre versus $7,453 per acre in the prior year period).

Improved Development sales of $12.2 million included $6.9 million from the Heartwood development project south of Savannah, Georgia and $5.3 million from the Wildlight development project north of Jacksonville, Florida. Sales in Heartwood consisted of a 101-acre parcel for $3.0 million ($30,000 per acre) sold to a national homebuilder for the first phase of an active-adult community, two residential pod sales totaling 62 acres for $1.8 million ($29,000 per acre), and 47 finished residential lots for $2.1 million ($44,000 per lot or $258,000 per acre). Sales in Wildlight consisted of a 97-acre parcel for $5.3 million ($55,000 per acre) sold to a national homebuilder for the second phase of an active-adult community. This compares to Improved Development sales of $11.6 million in the prior year period.

Rural sales of $15.6 million consisted of 3,411 acres at an average price of $4,582 per acre. This compares to prior year period sales of $23.4 million, which consisted of 4,633 acres at an average price of $5,054 per acre.

Timberland & Non-Strategic sales of $0.3 million consisted of a 76-acre transaction for $3,344 per acre. There were no Timberland & Non-Strategic sales in the prior year period.

Second quarter Adjusted EBITDA2 of $20.3 million decreased $5.1 million, or 20%, versus the prior year period.

Trading

Second quarter sales of $15.4 million decreased $12.3 million versus the prior year period due to lower volumes and prices. Sales volumes decreased 35% to 135,000 tons versus 209,000 tons in the prior year period. The Trading segment generated operating income of $0.1 million versus an operating loss of $0.4 million in the prior year period as improved margins more than offset reduced trading volume.

Second quarter Adjusted EBITDA2 of $0.1 million increased $0.5 million versus the prior year period.

Other Items

Second quarter corporate and other operating expenses of $10.3 million increased $0.2 million versus the prior year period, primarily driven by higher compensation and benefits expense ($0.8 million) and higher travel and transportation costs ($0.2 million), partially offset by lower legal expenses ($0.8 million).

Second quarter interest expense of $12.4 million increased $3.4 million versus the prior year period, primarily due to higher average outstanding debt and a higher weighted-average interest rate.

Second quarter interest and other miscellaneous income included an $11.4 million net recovery associated with a legal settlement.

Second quarter income tax expense of $0.2 million decreased $1.1 million versus the prior year period, primarily due to lower anticipated full-year results from our New Zealand subsidiary, which is the primary driver of income tax expense.

Outlook

“Based on our first half results and expectations for the remainder of the year, we now anticipate full-year net income attributable to Rayonier of $63 to $78 million, EPS of $0.42 to $0.52, pro forma EPS of $0.30 to $0.40, and Adjusted EBITDA of $275 to $300 million,” added Nunes.

“In our Southern Timber segment, we now expect full-year harvest volumes of 7.2 to 7.4 million tons as dry weather conditions have contributed to stronger-than-expected production levels. However, we anticipate lower quarterly harvest volumes for the remainder of 2023 compared to the first half of the year. We further expect a modest decline in weighted-average net stumpage realizations during the second half of 2023 compared to the second quarter driven by geographic mix and a seasonal increase in the proportion of thinning volume. We continue to anticipate higher non-timber income for full-year 2023 as compared to full- year 2022, driven by growth in our Nature-Based Solutions businesses. Overall, we expect the Southern Timber segment to generate full-year Adjusted EBITDA of $150 to $155 million, which at the midpoint is in line with our prior guidance.”

“In our Pacific Northwest Timber segment, we now expect full-year harvest volumes of 1.4 to 1.5 million tons as we have deferred some planned harvests in response to soft market conditions. We anticipate modestly higher weighted-average delivered log prices in the second half of 2023 compared to the first half based on improved end-market demand and lumber prices. Overall, we now expect the Pacific Northwest Timber segment to generate full-year Adjusted EBITDA of $30 to $34 million, a decline of $15 million at the midpoint versus prior guidance.”

“In our New Zealand Timber segment, we now expect full-year harvest volumes of 2.3 to 2.5 million tons as we have deferred some planned harvest volume in response to unfavorable market conditions. Over the balance of the year, we anticipate that weighted-average delivered log prices will be modestly lower as compared to the first half of 2023, primarily due to weaker demand in both export and domestic markets as well as increased supply from Cyclone Gabrielle salvage operations. However, we expect that lower port and freight costs will partially offset these headwinds. Further, while we have tempered our full-year expectations for carbon credit sales based on significant market volatility and limited transaction activity in the first half of the year, we expect to be more active in the carbon market in the second half of the year following the recent uptick in NZU pricing in response to governmental action to stabilize the market. Overall, we now expect the New Zealand Timber segment to generate full-year Adjusted EBITDA of $39 to $46 million, a decline of roughly $19 million at the midpoint versus prior guidance.”

“In our Real Estate segment, the demand for HBU properties and timberland assets has remained remarkably strong despite the higher interest rate environment. We now expect full-year Adjusted EBITDA of $90 to $100 million, an increase of roughly $23 million at the midpoint versus prior guidance. Based on the timing of anticipated closings, we expect that second half transaction volume and operating results in the Real Estate segment will be heavily weighted to the fourth quarter.”

For the complete press release, click here.

About Rayonier

Rayonier (NYSE:RYN) is a leading timberland real estate investment trust with assets located in some of the most productive softwood timber growing regions in the United States and New Zealand. As of September 30, 2022, Rayonier owned or leased under long-term agreements approximately 2.7 million acres of timberlands located in the U.S. South (1.79 million acres), U.S. Pacific Northwest (486,000 acres) and New Zealand (417,000 acres). More information is available at www.rayonier.com.

Contact:

Collin Mings – Media Contact – (904) 357-9100 – investorrelations@rayonier.com

Source: Rayonier, Inc.

The Value of Membership

As the leading provider of in-depth business and credit information on the domestic lumber & forest products industry, a membership with Blue Book Services gives you access to:

- Ratings & Business Reports

- Dynamic Search Tools

- Real-Time Data